Q2 Market Update

Peak Uncertainty, Prime Opportunity: Is Australia’s Property Market Entering Its Best Buying Window?

What I’m Watching This Month

Australia’s property market has shifted from momentum-led growth to a more selective, confidence-driven phase.

Higher rates, sticky underlying inflation, affordability pressure, weaker investor demand and negative gearing/CGT changes are all weighing on sentiment. But that is exactly why the current market deserves attention.

My view is that the indicators are pointing towards peak uncertainty, low confidence and the formation of a buying opportunity.

This is not because the market is risk-free. It’s because quality assets are starting to reprice at the same time the long-term fundamentals remain structurally supportive.

Markets Are Repricing, Not Breaking

Cotality’s latest Home Value Index shows national dwelling values were flat in May and up just 0.6% over the quarter, although still 8.8% higher over the year. Sydney is now 2.1% below its November 2025 peak, while Melbourne is 3.2% below its March 2022 peak.

For long-term buyers, that matters. Australia’s two deepest housing markets are no longer priced at peak exuberance. Sentiment has cooled, vendors are becoming more realistic, and buyers have more negotiating power than they did only months ago.

These markets are repricing, not breaking.

That distinction is important. A broken market is one where fundamentals collapse. A repricing market is one where confidence weakens, prices adjust, and better entry points begin to appear for disciplined buyers.

Negative Gearing Uncertainty Is Creating A Window

The announced negative gearing and CGT changes have added another clear layer of uncertainty.

From 1 July 2027, negative gearing will be limited to new builds, while existing arrangements remain unchanged for properties held before Budget night. The CGT discount is also being replaced with an inflation-based discount, alongside a minimum 30% tax on gains from 1 July 2027.

Markets often misprice assets during policy transitions. Some investors pause, others overreact, and many wait for absolute clarity. That adjustment period can create opportunity for buyers who understand the fundamentals.

If investor demand temporarily weakens, quality established assets may become easier to negotiate on, even as the underlying market fundamentals continue to point in the right direction.

Supply Is Still The Major Constraint

The strongest support for the market remains a critical housing undersupply.

The National Housing Accord target is 1.2 million new homes over five years from 1 July 2024… equal to roughly 240,000 homes per year, or 20,000 per month.

Yet ABS building approvals fell 3.4% in April to 16,710 dwellings. That is materially below the run-rate required to meet the national target, and approvals are only the first step before construction and completion. With new dwelling construction costs again one of the stronger contributors in the latest CPI release, the outlook for a meaningful lift in housing completions remains grim. Higher build costs continue to pressure developer feasibility, slow new project commencements and make it harder for the market to deliver the level of supply needed to ease the undersupply problem.

Demand can soften quickly, but supply takes years to fix.

If Australia is already falling behind on approvals, the undersupply problem is unlikely to resolve soon. That creates a floor under well-located housing markets, especially in areas supported by jobs, infrastructure, population growth and rental demand.

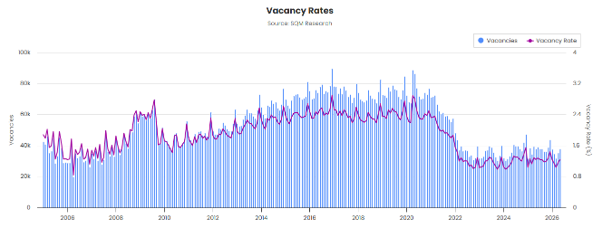

Rental Pressure Is Reinforcing The Floor

SQM Research shows the national vacancy rate holding at just 1.2% in May, with national asking rents up 7.8% over the past 12 months.

This is not a balanced rental market. It is a market still operating under severe supply side pressure.

For investors, the implication is important. While prices have stabilised or softened in parts of the market, rents are rising… and will continue to do so. That means yields are improving.

In a market where buyer sentiment is weak but rental demand remains strong, the risk-reward profile begins to shift back towards disciplined acquisition. That does not mean every asset is attractive. But well-located housing in tight rental markets remains supported by one of the most powerful fundamentals in Australian property - people still need somewhere to live, and there is not enough stock.

Inflation Is Easing, But Underlying Pressure Remains

Oil has moved in the right direction for inflation, with crude down roughly -38% to around US$69 per barrel following positive peace talks between the USA and Iran. If sustained, this will ease pressure on fuel, freight and transport costs, helping pull inflation lower.

Softening house prices also add to that disinflationary pressure, despite not being recorded in the CPI basket. If property prices keep softening, the negative wealth effect could make households more cautious, delay spending and reduce demand across the economy.

That matters because the latest CPI print is already moving in the right direction. Annual inflation fell to 4.0% in May, down from 4.2% in April. Headline inflation is easing, fuel inflation is cooling and demand appears to be softening.

The caveat is trimmed mean inflation, which rose to 3.6% from 3.4%, showing underlying pressure has not fully rolled over yet. That means rate cuts may not be immediate. But the market does not need immediate cuts to stabilise. It simply needs confidence that the worst is behind us - and that shift is already showing up, with markets no longer pricing in further hikes and increasingly treating the current cash rate as the likely peak. We're not at target yet, but direction matters as much as level.

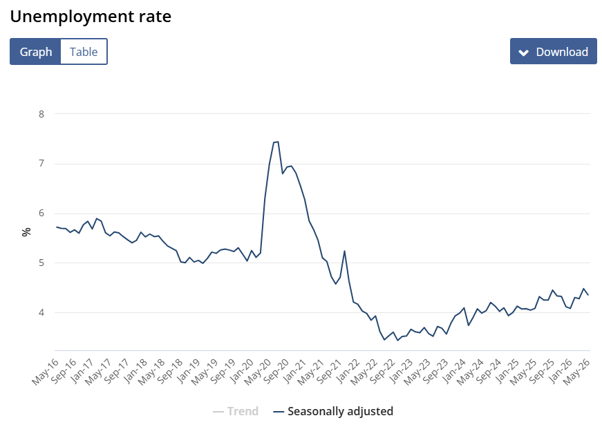

The Labour Market Is Softer, But Not Broken

Unemployment eased from 4.5% in April to 4.4% in May - suggesting that the labour market still has some resilience. However, unemployment has been on the rise sine 2022 and remains much higher than this time last year.

That makes the next few months important. If unemployment continues to rise and inflation continues to ease, the RBA’s tone could shift quickly.

Rate cuts aren’t my base case just yet, but the case for further hikes is weakening.

Unemployment rate over the past 10 years

What these means for you

This is the first market in a while where buyers have a genuine opportunity to act with more control.

For those waiting on the sidelines, this is the period to pay attention. The best buying windows rarely feel obvious in the moment. They usually appear when uncertainty is high, confidence is low, yet the fundamentals remain strong.

That is where the market is today.

Sydney and Melbourne have already repriced from their peaks. Negative gearing and CGT changes are disrupting investor behaviour. Higher rates have weakened confidence. Yet inflation is easing at the headline level, oil prices have pulled back, unemployment is rising and markets are increasingly treating the current cash rate as the likely peak of the cycle.

The structural case remains strong. Building approvals are still below the level required to meet housing targets, vacancy rates remain extremely tight and rents are still rising.

That is where the opportunity sits. Not in assuming every market rebounds immediately, and not in buying anything simply because it has fallen in price. But in recognising that quality assets in undersupplied, high-demand locations are now more negotiable while the long-term fundamentals remain intact.

The risk is waiting until everyone feels confident again. By then, the opportunity may already be gone. The market is not breaking. It’s repricing. And for buyers with a long-term gameplan, that repricing is creating one of the most compelling entry points of the cycle.