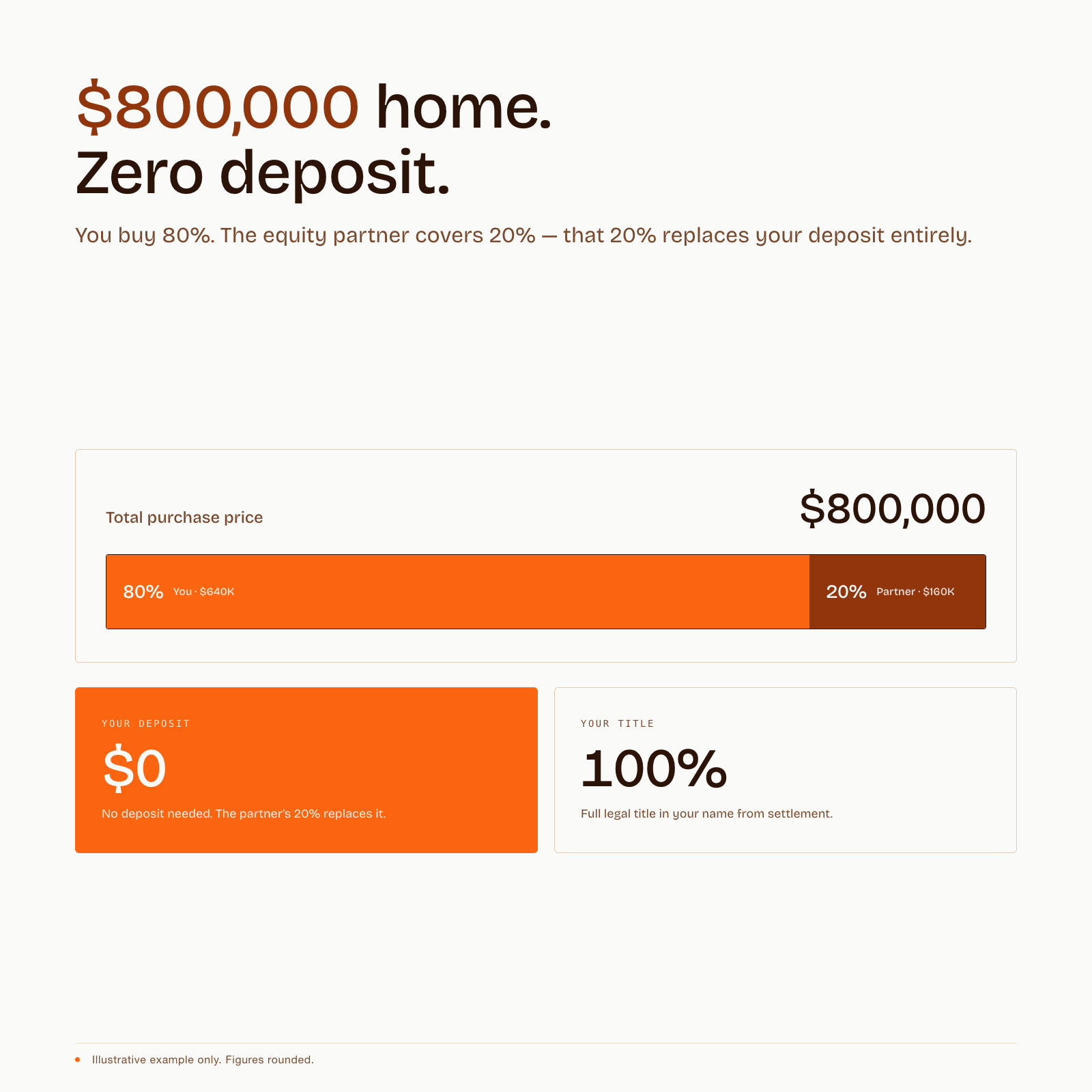

Own your home with Zero Deposit*

A structured five-year pathway to full ownership on select apartments.

The Problem

You can afford the mortgage. You just can’t save the deposit.

$800

Average weekly rent

That’s $41,600/year going to your landlord. Every year of rent is a year building

someone else’s equity.

$160,000

Typical deposit needed

On an $800K home with

20% deposit. The maths doesn’t

work for most people.

$0

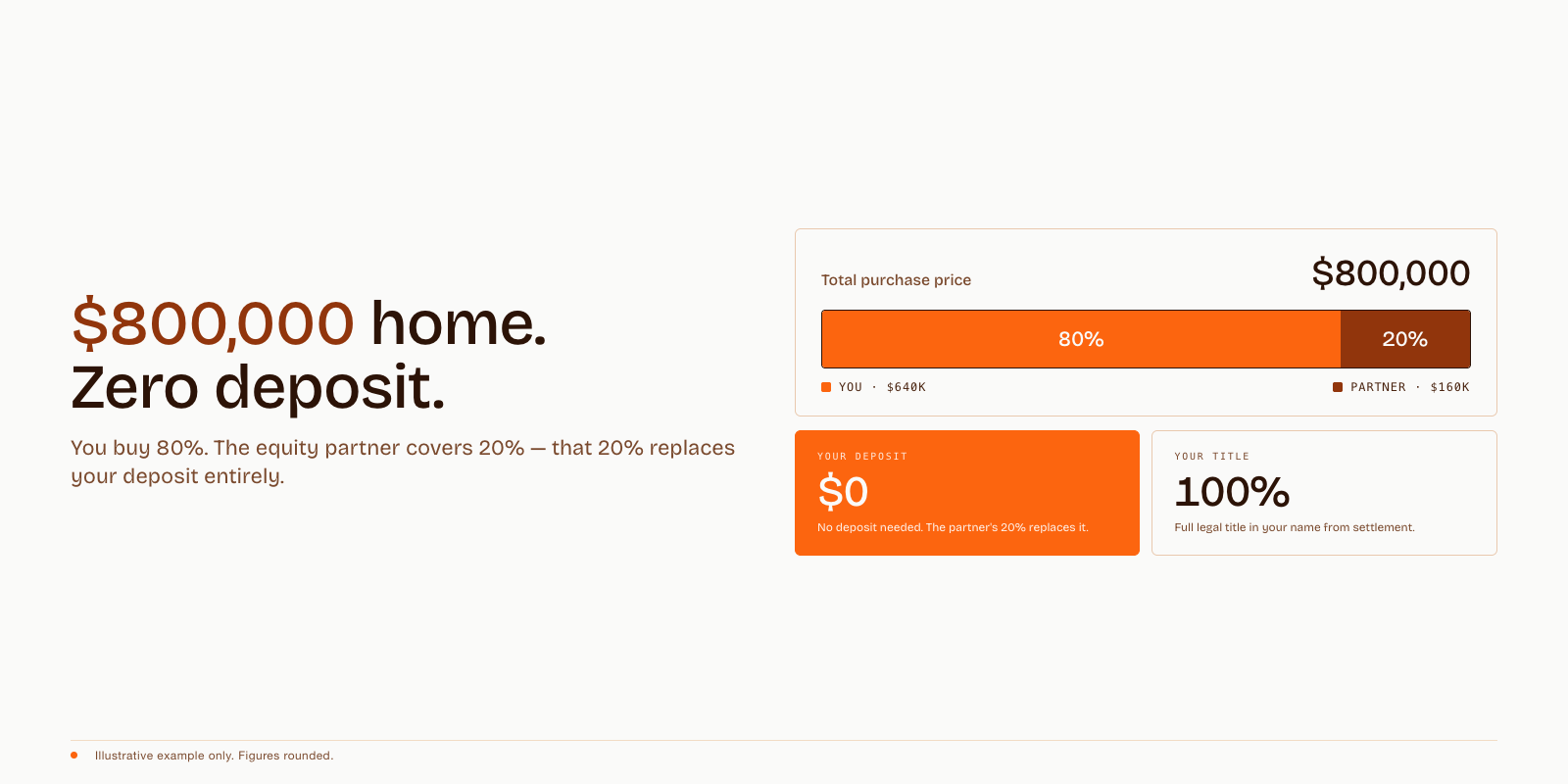

Deposit with Shared Equity

The equity partner’s 20% replaces

your deposit entirely.

Full legal title from day one.

How it works

Clear about what this is and what it isn’t

This is NOT

✗ A government grant or subsidy

✗ Rent-to-own or lease-to-buy

✗ Co-ownership: the partner NOT on title

✗ Social or subsidised housing

✗ Available on any property

This IS

✓ A private-market shared equity arrangement

✓ Zero deposit, the equity partner's 20% replaces it

✓ Full legal title in your name from settlement

✓ Financing Available

(Lender partners already in place)

✓ A clear five-year pathway to complete ownership

✓ Available on select new Equitifund homes in Sydney and Melbourne

Who can apply?

People 18 years

or older

Australian citizen or

permanent resident

Qualify for home loan through approved

lender partners

Intend to live in

the property

as principal residence

Frequently Asked Questions

-

Exactly what it sounds like. The equity partner puts in 20% of the purchase price and that replaces your deposit completely. You don't need to bring a cent for the deposit. You will still pay the normal costs that come with any property purchase, like legal fees and stamp duty, but the deposit itself is zero.

-

No. Your name goes on the title. Theirs doesn't. They hold a financial interest that's secured against the property. Think of it like a second mortgage that gets paid out over time. They have zero say in how you live, what colour you paint the walls, or who comes over for dinner.

-

You need to buy out the equity partner's remaining share by year five. But you don't have to wait. You can start buying them out from day one, in chunks as small as 5% at a time. Most people refinance to complete the buy-out. If for some reason you can't buy them out by year five, the property may need to be sold and the proceeds are split based on each party's share.

-

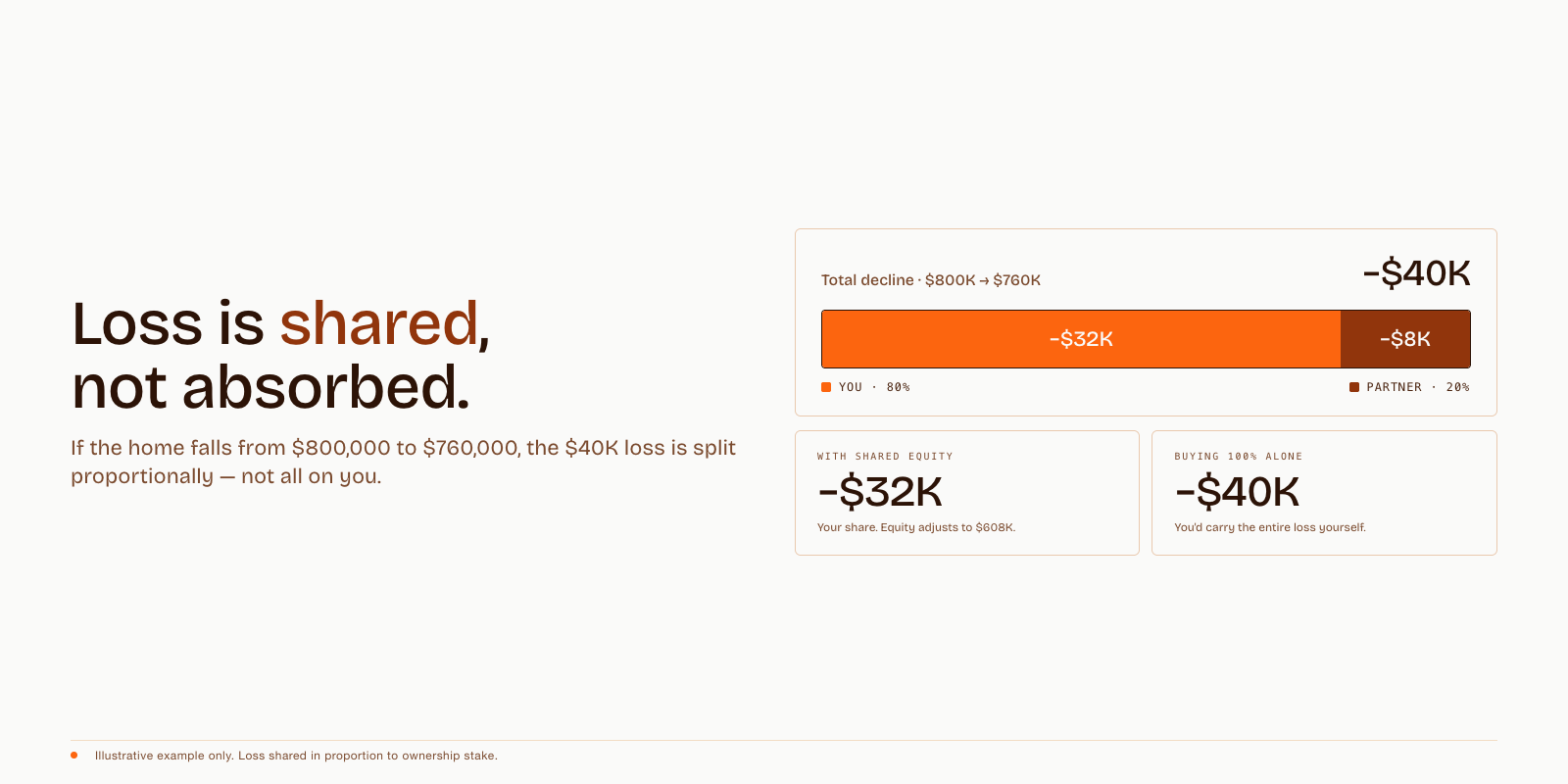

You're not on your own. The loss is shared proportionally. If you own 80% and the property drops, you absorb 80% of the decline and the partner absorbs 20%. That's one of the key advantages over buying 100% traditionally, where you'd carry the entire loss yourself.

-

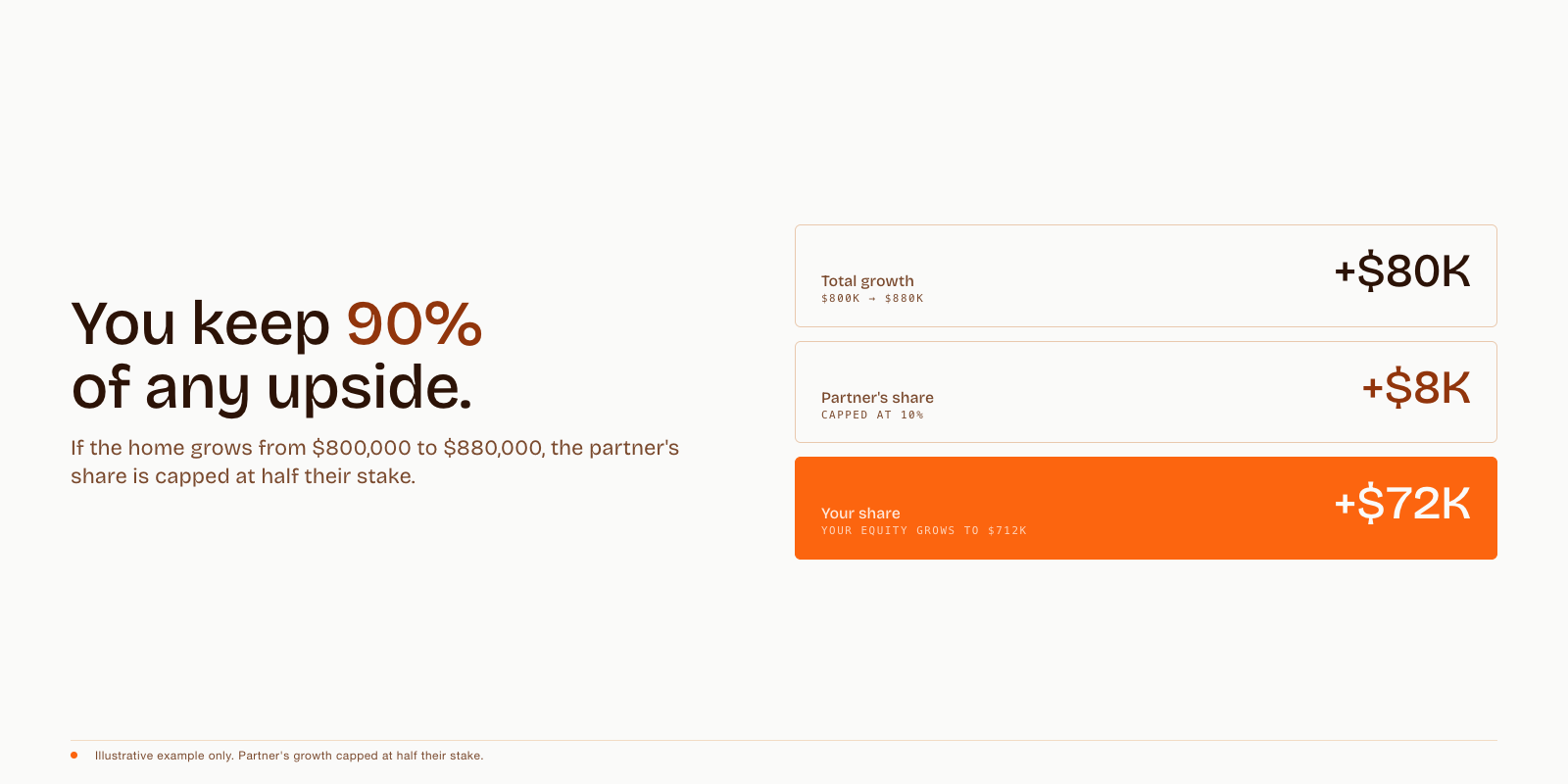

This is where the structure really works in your favour. Growth is shared, but the partner's share is capped at half their percentage. So if they hold 20%, they can only claim 10% of any increase. On an $80,000 gain, they'd get $8,000 and you'd keep $72,000. The longer you hold, the more the maths favours you.

-

No, and this is a big deal. Lender partners are already set up and familiar with the shared equity structure. You don't need to shop around trying to explain the arrangement to banks who've never seen it before. We connect you with the right lender as part of the process.

-

No. This only applies to select new properties delivered by Equitifund, not any home on the open market. That's how we're able to structure the zero-deposit arrangement. Our team can show you exactly what's currently available.

Ready to stop renting and start owning?

Book a free, no-obligation call. We’ll walk you through the pathway, check eligibility, run the numbers.